S&P 500 Joiners & Leavers: The Index Curse Fact-Checked

We often discuss whether it's worth buying stocks that are newly added to the S&P 500. The thesis: ETFs have to buy on the key date, so the price must rise. I ran the data against this – specifically from the moment the stock is actually in the index.

The Mechanics (Announcement vs. Inclusion)

Announcement Date: S&P announces the inclusion. This is where the front-run begins, traders buy ahead of index tracking. Effective Date (Day 0): The stock is physically included, the large ETF buying volume is already in the market.

Part 1: S&P 500 Joiners

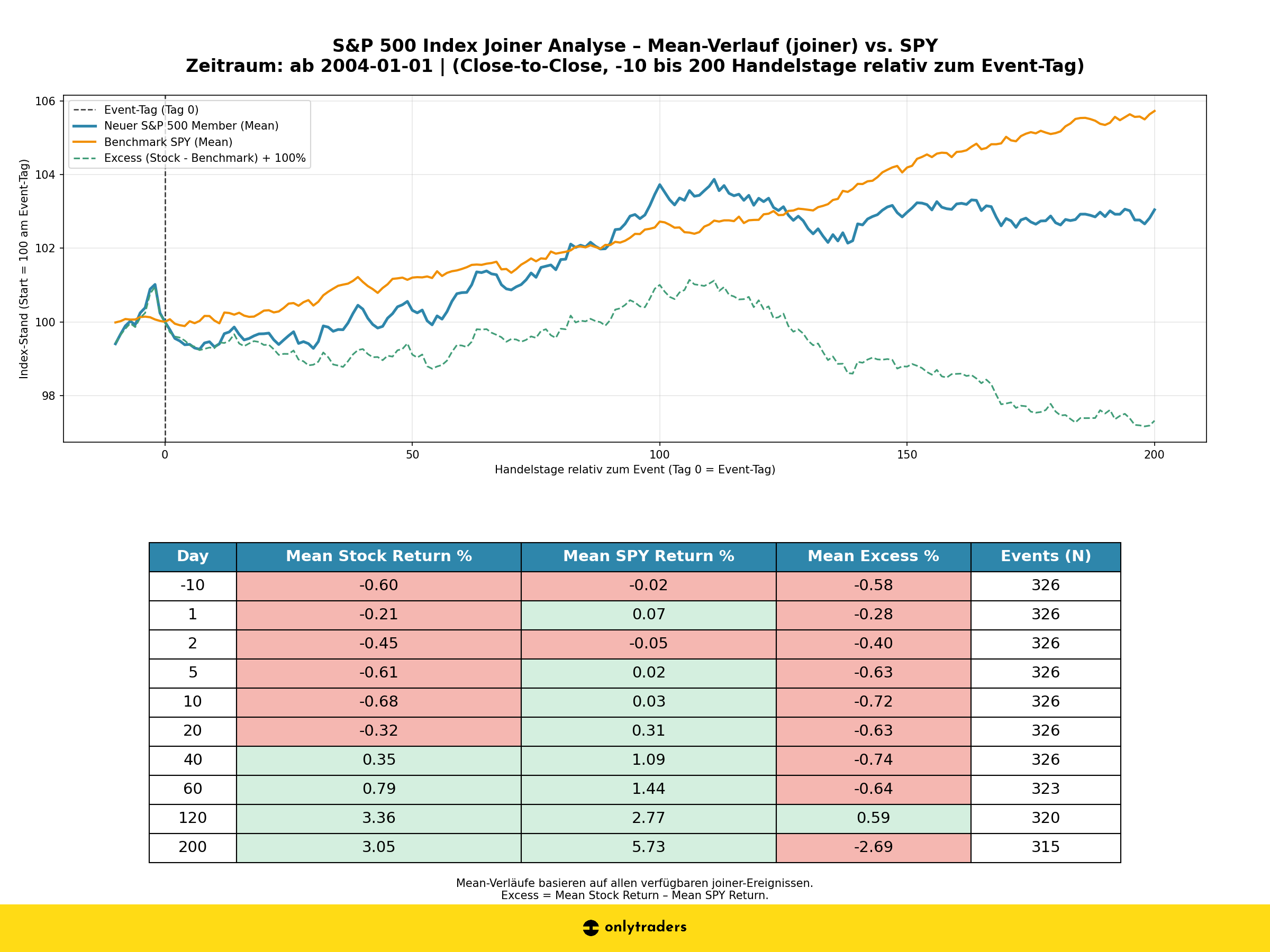

The Big Picture (2004 – today)

Base: 444 Events · Benchmark: SPY

Immediately after inclusion, we see red. On Day 10, joiners are already lagging -0.68% behind SPY on average. Long-term, the excess return collapses permanently: After 200 trading days, the underperformance is -2.69%. Interpretation: The ETF liquidity on Day 0 is used to unload positions. Buyers on the inclusion day are often exit liquidity for arbitrageurs.

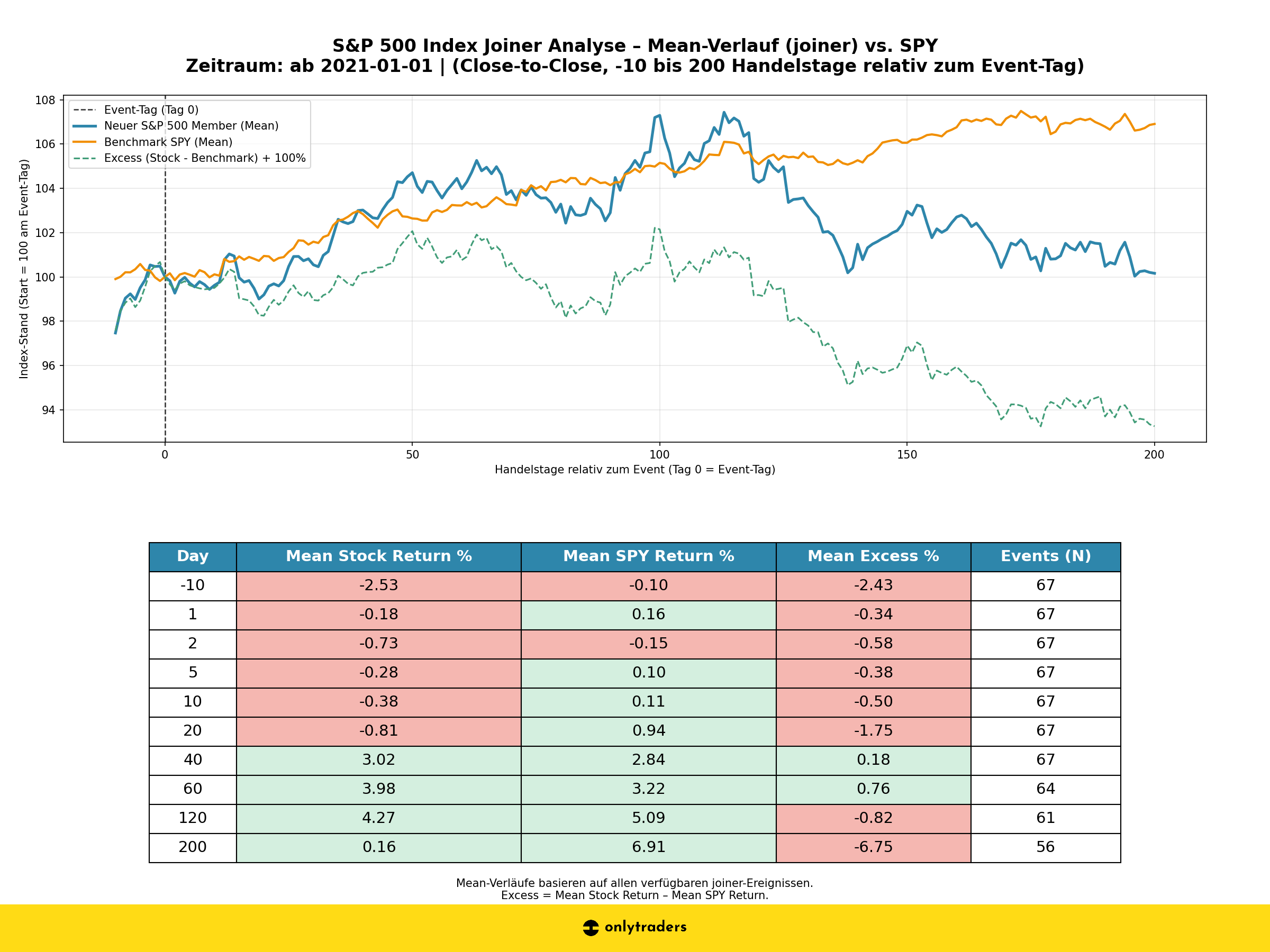

The Modern Era (since 2021)

Base: 67 Events (last ~4 years)

Since 2021, the effect has been more brutal. On Day 20, we are at -1.75% excess (previously approx. -0.6%). Between Day 40–60, a bull trap occurs, then the trend tips downwards again. After 200 days: -6.75% excess – that's almost 7% worse than the index they were just added to.

Conclusion & The Edge (Joiners)

- Stay away on inclusion day: Buy the Rumor, Sell the News is statistically confirmed.

- Short potential: Especially since 2021, selling pressure after inclusion is massive.

- The edge is not on the long side, but in the sell-off after Day 0.

Part 2: S&P 500 Absteiger (Leavers)

In Part 1 we see: Joiners fall after inclusion. The question is: Do leavers then have to rise? Old doctrine says: Mean Reversion. The data since 2021, however, shows a structural break.

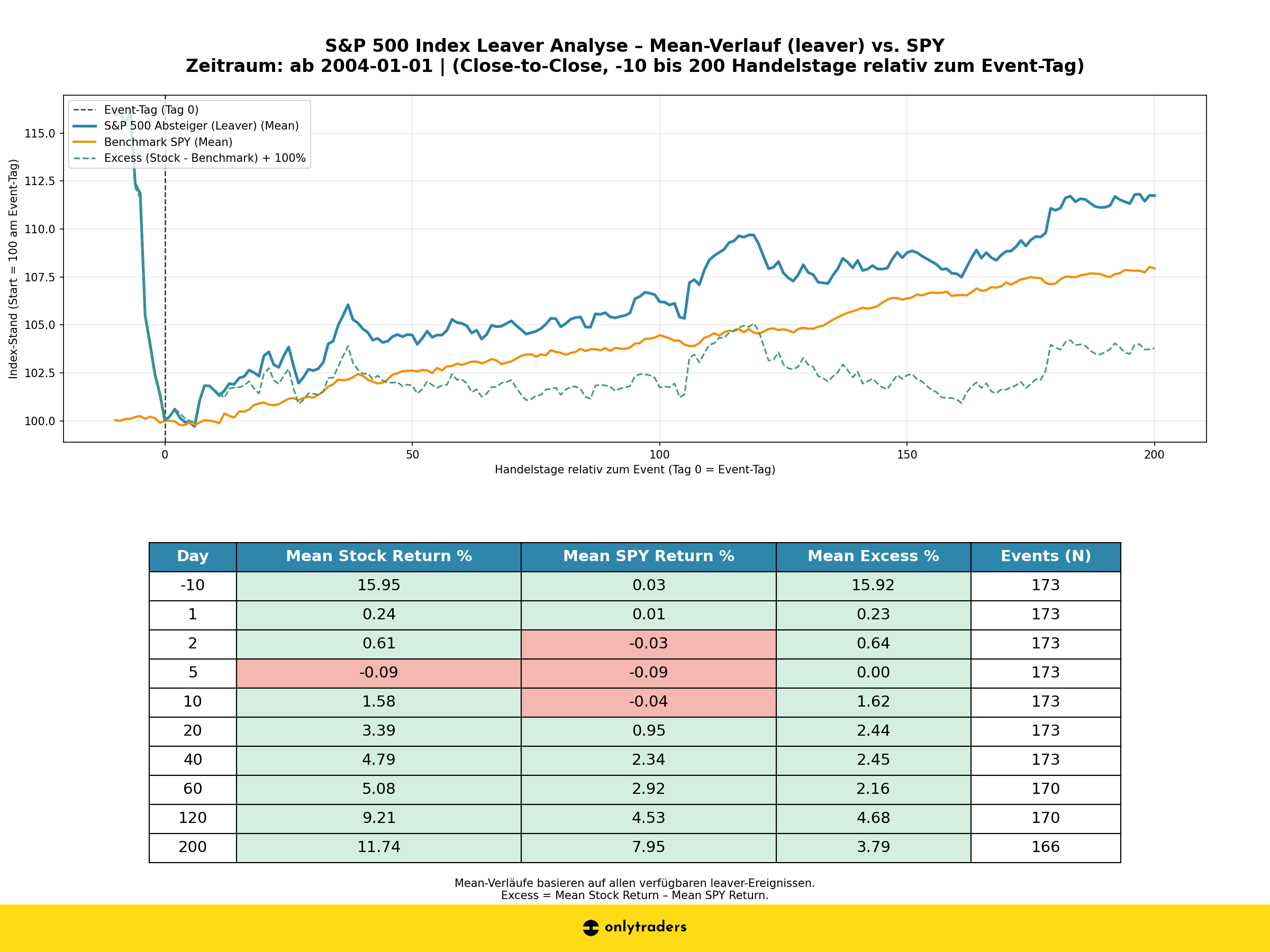

The Big Picture (2004 – today)

Base: 166 Events (after 200 days) · Benchmark: SPY

Historically, prices stabilize after being kicked out. After 200 days, leavers actually beat the index by +3.79%. For bargain hunters, this was a valid strategy for a long time.

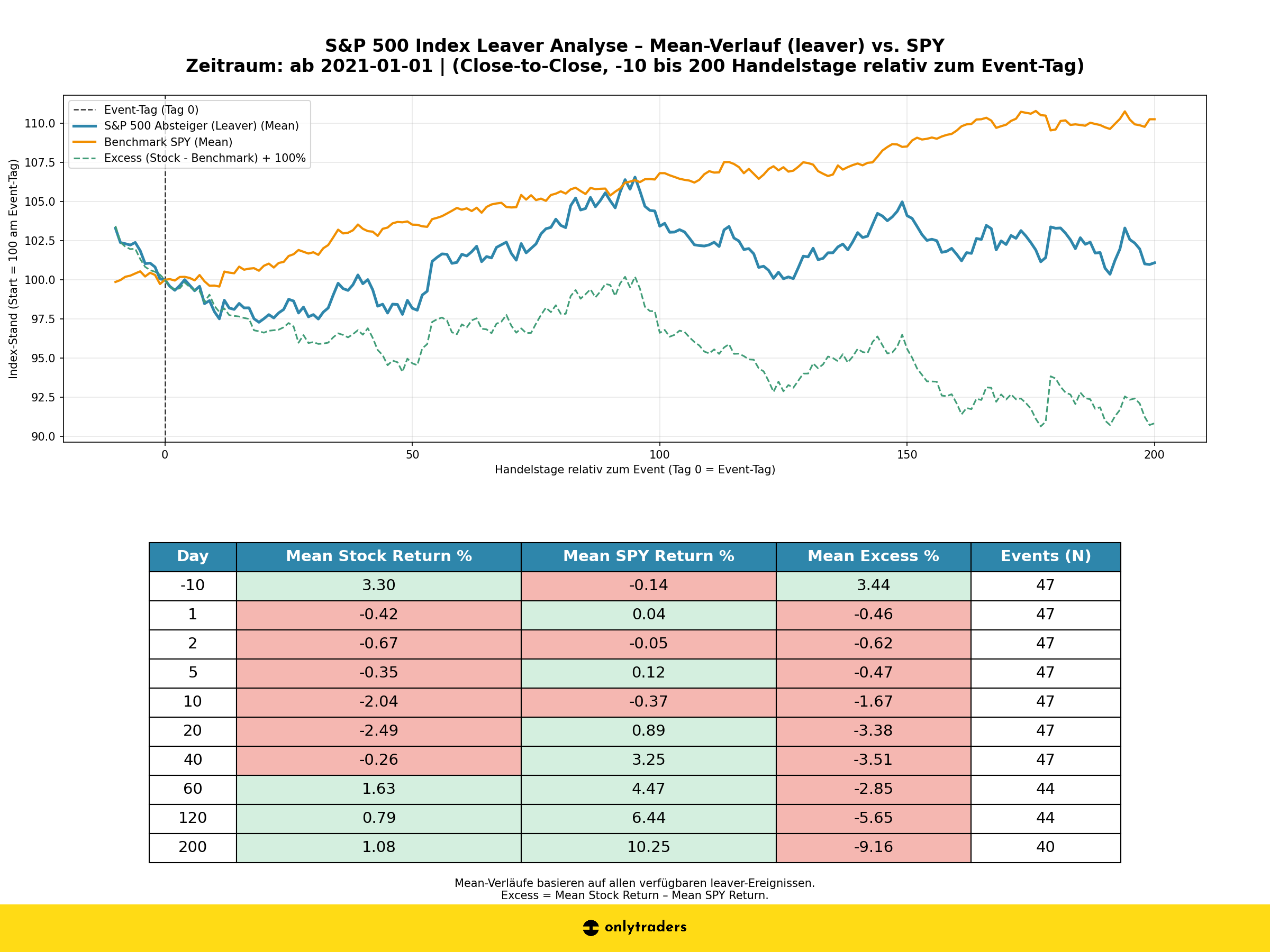

The Modern Era (since 2021)

Base: 40 Events (after 200 days)

Since 2021, the knife keeps falling. After 200 days, leavers are at -9.16% excess. The trend channel is almost linearly downwards. The supposed value play is toxic today.

Conclusion & The Edge (Leavers)

- Value fishing no longer works since 2021. Many companies are becoming obsolete.

- Don’t catch the knife: No discount, but "Toxic Waste".

- Short side remains attractive (Day 20 to Day 200).

Nerd Knowledge: Why is the database smaller?

Many departures are acquisitions (M&A). These delistings fall out because 200 post-event days are needed. Additionally, there describe data matching problems (ticker changes, Norgate vs. Polygon). This reduces the quantity, but the downward trend remains robust and statistically clear.