Friday the 13th on the Stock Market: Curse or Blessing?

Today is Friday the 13th – and because we love data, we asked the question: Do SPY, QQQ, and the DAX really perform worse on this „unlucky day"? Spoiler: The superstition doesn't hold up against the data.

The Idea

Friday the 13th is considered an unlucky day in pop culture. Some traders avoid the day, others trade as usual. We isolated every Friday the 13th since 2004 and compared them against the benchmark (all trading days in the same period) — for the US (SPY, QQQ) and Germany (DAX). We measured the daily return in two ways: Open‑to‑Close (O2C) and Close‑to‑Close (C2C, i.e. from the previous day’s close).

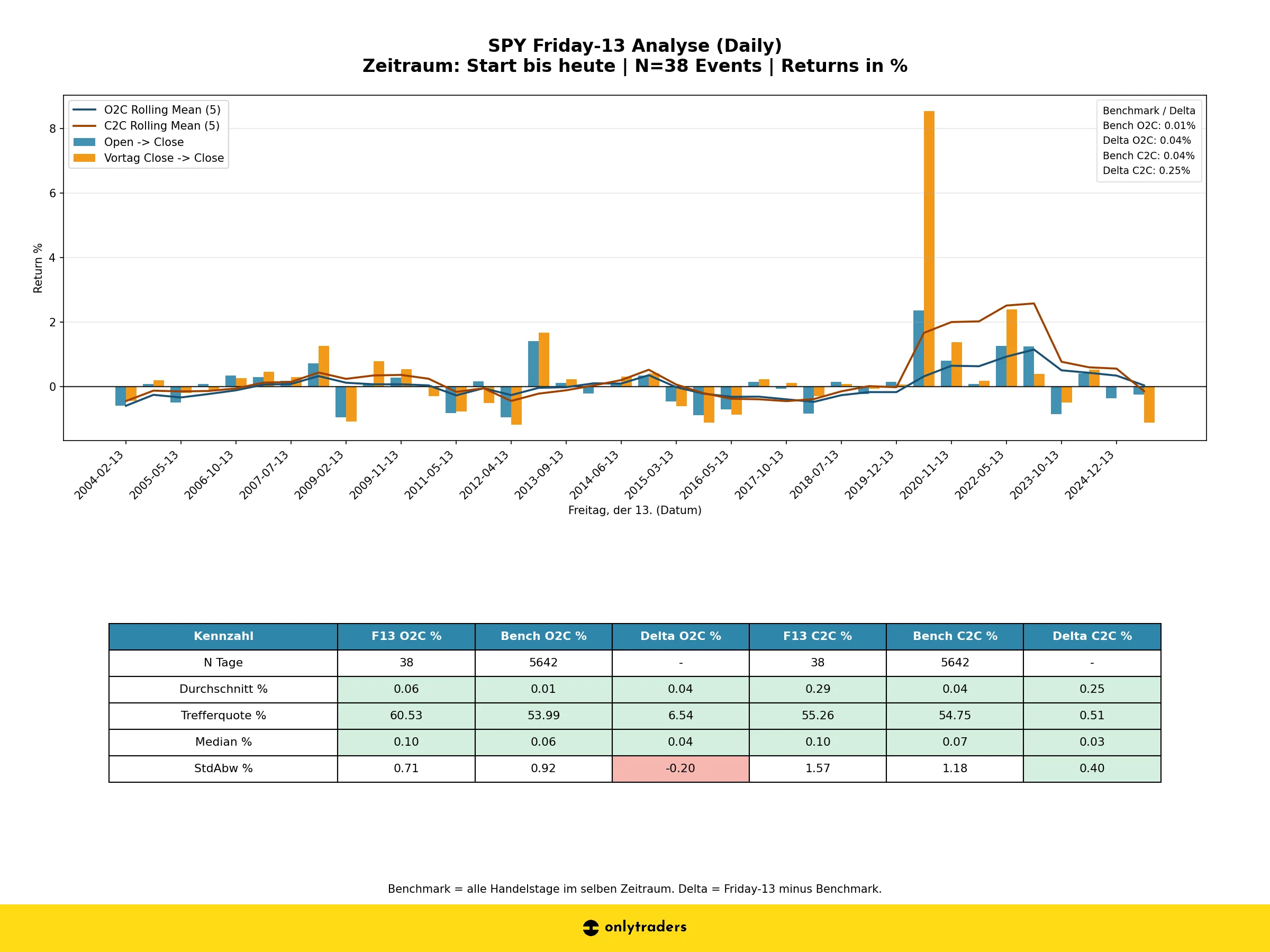

SPY: S&P 500 on Friday the 13th

Base: 38 events · Benchmark: 5,642 trading days

| Metric | F13 | Benchmark | Delta |

|---|---|---|---|

| Average O2C | +0.06% | +0.01% | +0.04% |

| Average C2C | +0.29% | +0.04% | +0.25% |

| Hit rate O2C | 60.53% | 53.99% | +6.54% |

| Hit rate C2C | 55.26% | 54.75% | +0.51% |

| Median O2C | 0.10% | 0.06% | +0.04% |

| Median C2C | 0.10% | 0.07% | +0.03% |

SPY delivers a slightly better average return on Friday the 13th than on normal days — both intraday (+0.04% delta) and overnight (+0.25% delta). The hit rate O2C at over 60% is even significantly higher than the benchmark (54%).

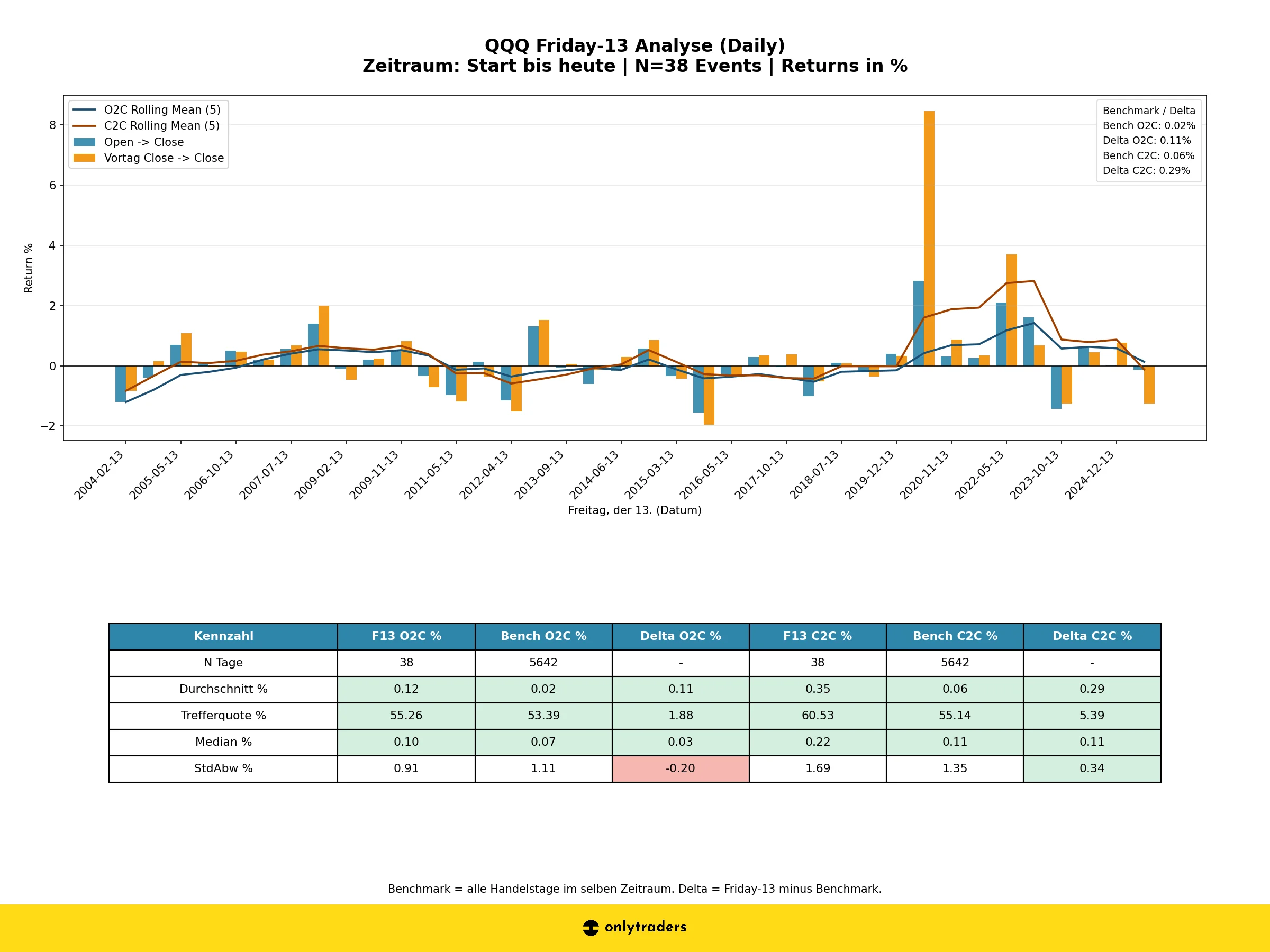

QQQ: Nasdaq 100 on Friday the 13th

Base: 38 events · Benchmark: 5,642 trading days

| Metric | F13 | Benchmark | Delta |

|---|---|---|---|

| Average O2C | +0.12% | +0.02% | +0.11% |

| Average C2C | +0.35% | +0.06% | +0.29% |

| Hit rate O2C | 55.26% | 53.39% | +1.88% |

| Hit rate C2C | 60.53% | 55.14% | +5.39% |

| Median O2C | 0.10% | 0.07% | +0.03% |

| Median C2C | 0.22% | 0.11% | +0.11% |

QQQ shows an even clearer picture: +0.29% C2C delta versus the benchmark. The Close‑to‑Close hit rate is over 60% — that’s solid. The Nasdaq seems to like Friday the 13th rather than fear it.

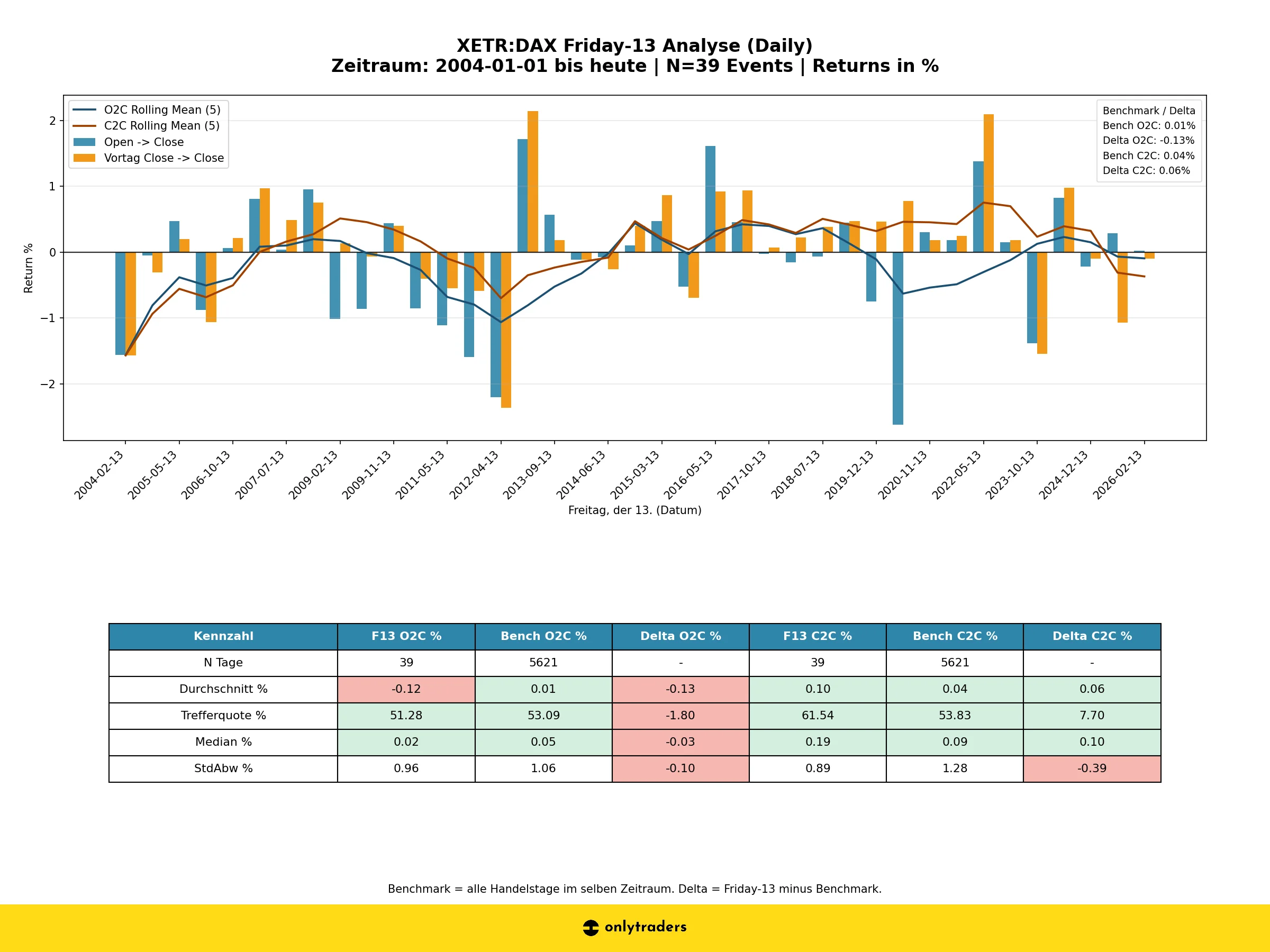

DAX: The German Market on Friday the 13th

Base: 39 events · Benchmark: 5,621 trading days

| Metric | F13 | Benchmark | Delta |

|---|---|---|---|

| Average O2C | −0.12% | +0.01% | −0.13% |

| Average C2C | +0.10% | +0.04% | +0.06% |

| Hit rate O2C | 51.28% | 53.09% | −1.80% |

| Hit rate C2C | 61.54% | 53.83% | +7.70% |

| Median O2C | 0.02% | 0.05% | −0.03% |

| Median C2C | 0.19% | 0.09% | +0.10% |

The DAX gets interesting: intraday (O2C), Friday the 13th actually shows slight weakness with a −0.13% delta. But: look at Close‑to‑Close, and the picture flips. The C2C hit rate on F13 is over 61% — almost 8 percentage points above the benchmark. So the „curse” only hits the DAX intraday at most — overnight, more than compensated.

Conclusion: No Curse, More Like a Mini Edge

- Myth busted: Friday the 13th is not a bad trading day. Neither SPY nor QQQ show underperformance — and the DAX makes up everything overnight.

- US clearly positive: SPY and QQQ even perform slightly better on F13 than the average of all days.

- DAX special case: Slightly negative intraday (−0.13% O2C delta), but the C2C hit rate of 61.5% is impressive.

- Not tradable: With ~38 events and deltas in the 0.04–0.29% range, this is statistically thin. Not a strategy — but a clean proof that the superstition is nonsense.

- Fun fact: The standard deviation (volatility) on F13 days is actually lower than normal for SPY. So the day isn’t just not bad, it tends to be calmer.

So: no reason to shut down the computer on Friday the 13th. Trading as usual even gives you a tiny statistical edge.