+8.6% in June — No Sign of a Summer Lull

June, start of summer — the S&P 500 and Nasdaq 100 drifted somewhat lower amid heavy swings. Our strategy mix delivered another solid month. Here's the honest monthly update: how our real-money portfolio performed in June, which trade worked best and which worst.

The Big Picture

Important context, as always with us: neither we as the two founders nor our community are demo heroes. We’re always talking about real results, not theoretical backtests. Slippage, commissions and the odd lesson from the constant learning process are already baked into the numbers. I personally (Michael) currently run our strategy mix across three accounts:

- the momentum strategy (our NDX Surfer) has been running for a while at FreeStoxx (commission-free real shares),

- the 1% per Week strategy on the Nasdaq 100 and the TGIM strategy on the S&P 500 via CFDs at Blackbull Markets (CFDs with no financing costs for the first 5 days, via ref link), and

- all the other strategies in the multi-market account at WHS (stocks, futures, ETFs… 10% off commissions via ref link)

Account sizes follow member surveys to reflect the broadest common ground. The MM account was funded with EUR 20,000, the CFD account with EUR 5,000, and the momentum positions at FreeStoxx are likewise scaled down to a EUR 5,000 start (they’ve been running for me since early 2025).

Everyone can and should trade where they feel comfortable — this is just my current setup. And it will keep evolving.

The Month in Numbers

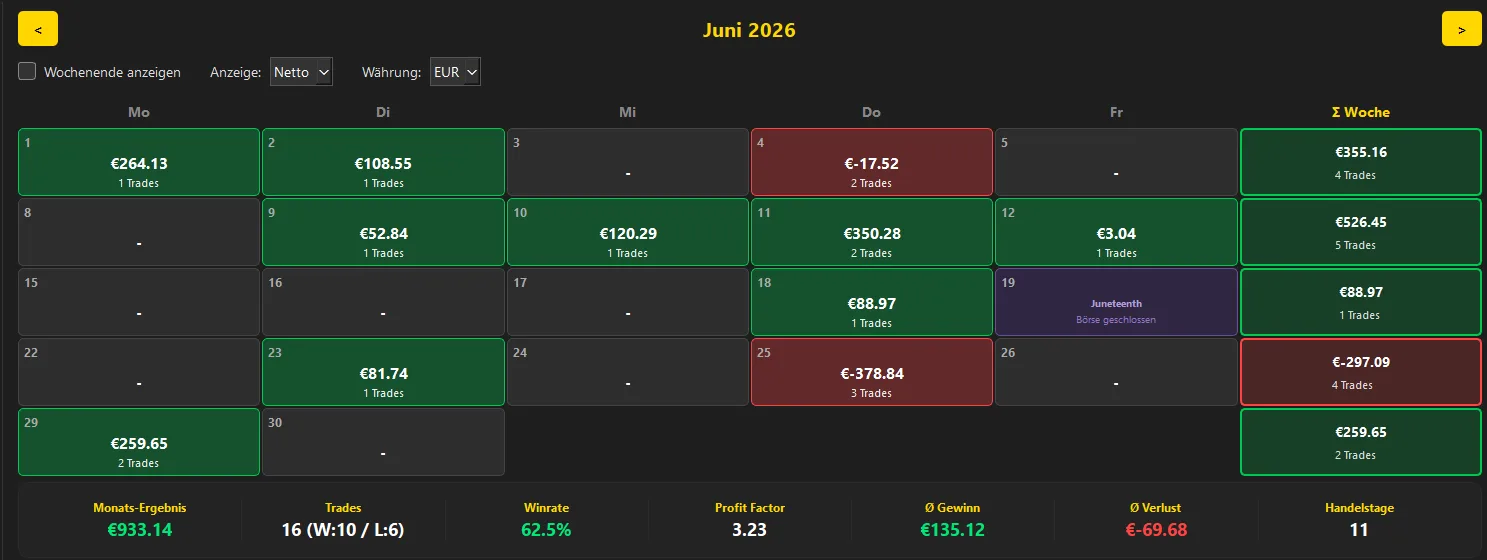

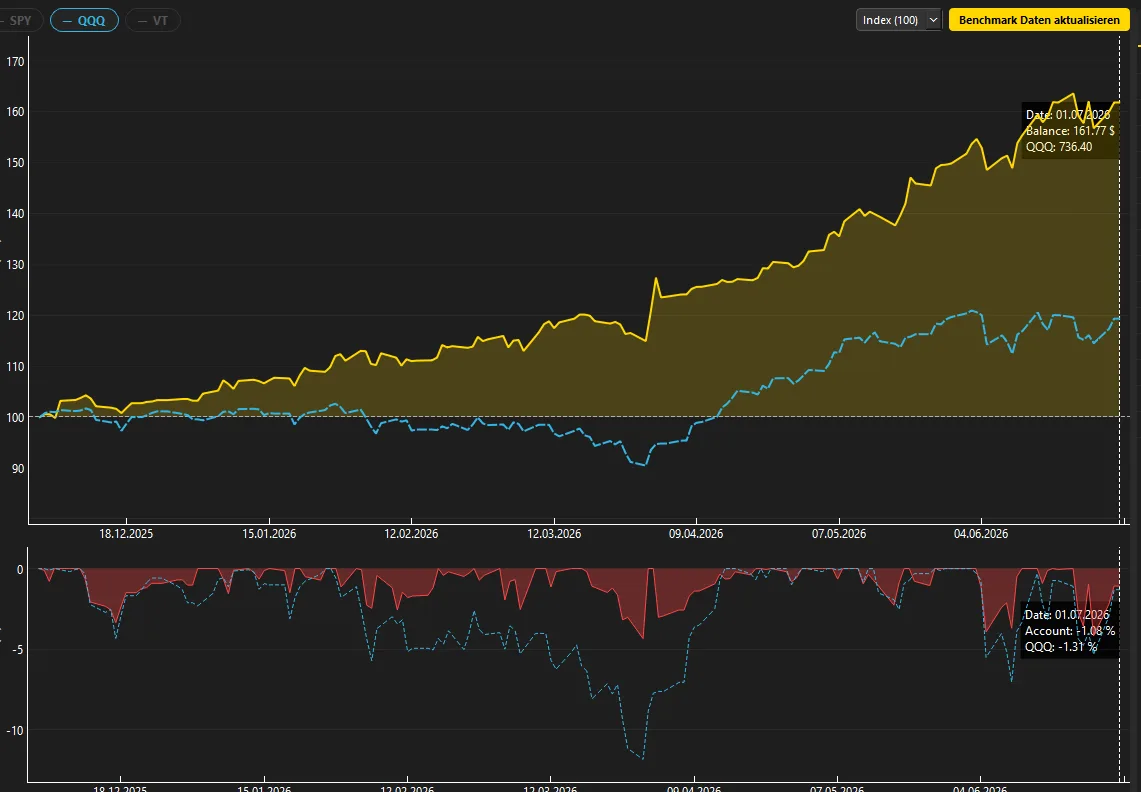

After 16 trades closed in June, our real-money strategy mix across all three accounts posted a realized monthly return of EUR 933, or +8.6%. The S&P 500 came in at -1.55% over the same period. The hit rate was 62.5% at a profit factor of 3.23.

That also made it the 7th green month in a row, and our strategy mix now stands at 55% YTD vs. +9.4% YTD for the benchmark S&P 500. And still at a markedly lower maximum drawdown than the index (-4.3% vs. -9.1%).

The Good

The best closed trade of the month in absolute terms was the Discount Sniper long in Rocket Lab (RKLB) at +281 EUR. A nice catch of the falling knife (mean reversion), and after a poor first day we quickly took profits again. The exit doesn’t look optimal. But with these MR strategies, aggressive targets work best over the long run.

In relative terms, the best closed trade was the exit from the NDX Surfer long in Intel (INTC) early in the month. Doesn’t look like much, and it had been sitting a lot higher before it got kicked out. But it still turned into +17.4%.

The Bad

No gains without losses in trading. That would be like a business with no material or staff costs. The one that stands out here is the Discount Sniper long in SLB at -273 EUR, or -7.4%. The time stop put an end to this attempt before the stock dropped even further.

Losers don’t hurt as long as they stay within the rules. That’s exactly why we build a mix of strategies that are as uncorrelated as possible over the long run: when a market phase isn’t ideal for one strategy, it fits another perfectly well.

The Ugly

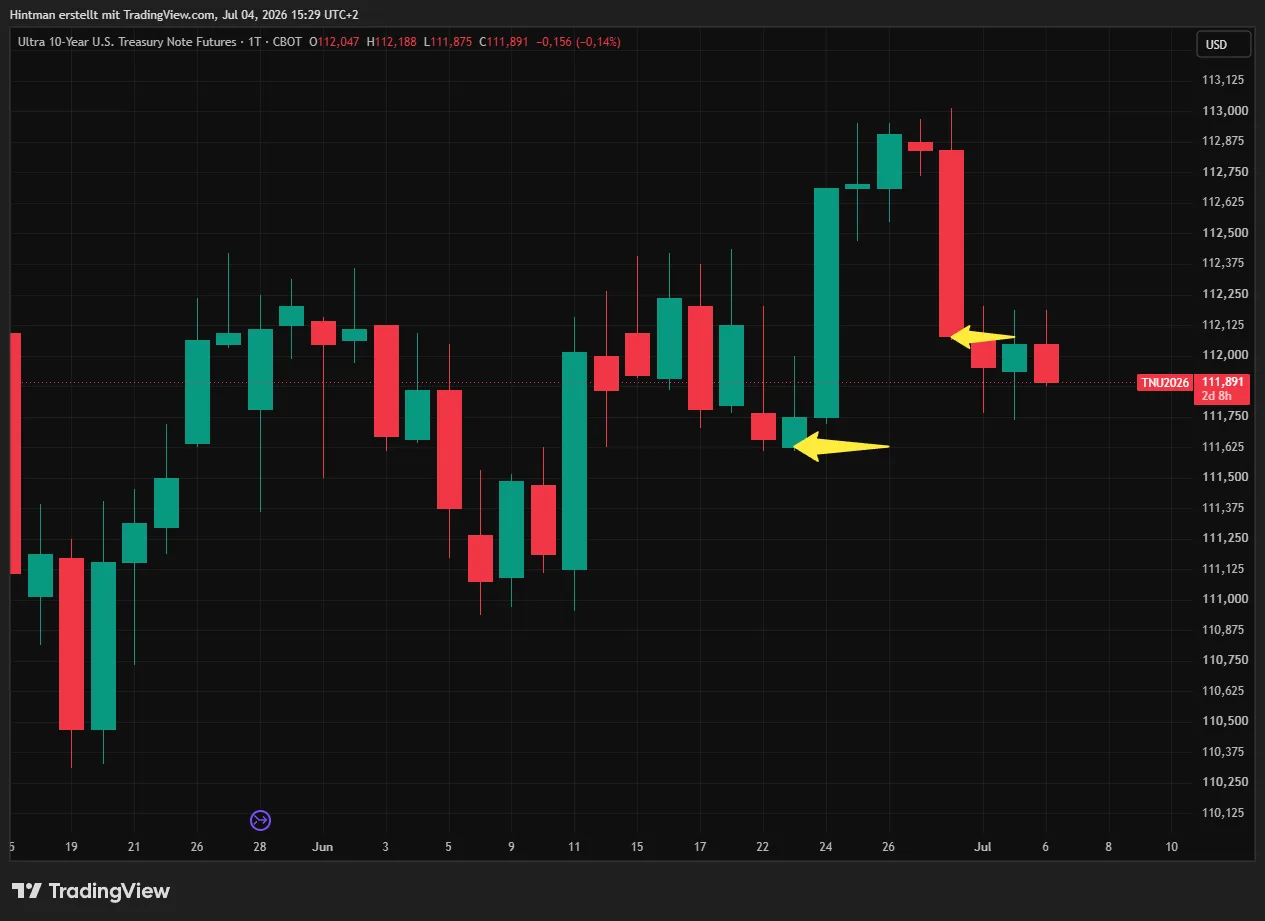

After May, our Seatreas strategy stayed quiet and inactive in June too. Supposedly. Friday, June 19 was a US market holiday. You’ll find that on every finance site — for example, neither Yahoo Finance nor TradingView shows a regular daily candle for the US T-Note future under the tickers TN, MTN or ZN.

Only when you switch to the intraday chart and change from regular to electronic trading hours do prices suddenly appear, running until 7 p.m. instead of the usual 11 p.m. Those are the Globex prices.

Had we known or noticed that in time (a big conditional), our rulebook would have allowed an entry on Tuesday. The bond price then ran up sharply afterwards. But on the last day of the month — and therefore on the exit day — it came back so clearly that Matthias and I shrug it off in hindsight.

So this potential ghost trade never was one, due to the missing regular trading hours — and nobody in the community threw it into the ring either.

July Outlook

We’re still waiting on the 1st trade in our newest strategy Thank God It’s Monday, and on top of that at least one more methodology is coming — one meant to cushion our long-US-equity tilt a bit.

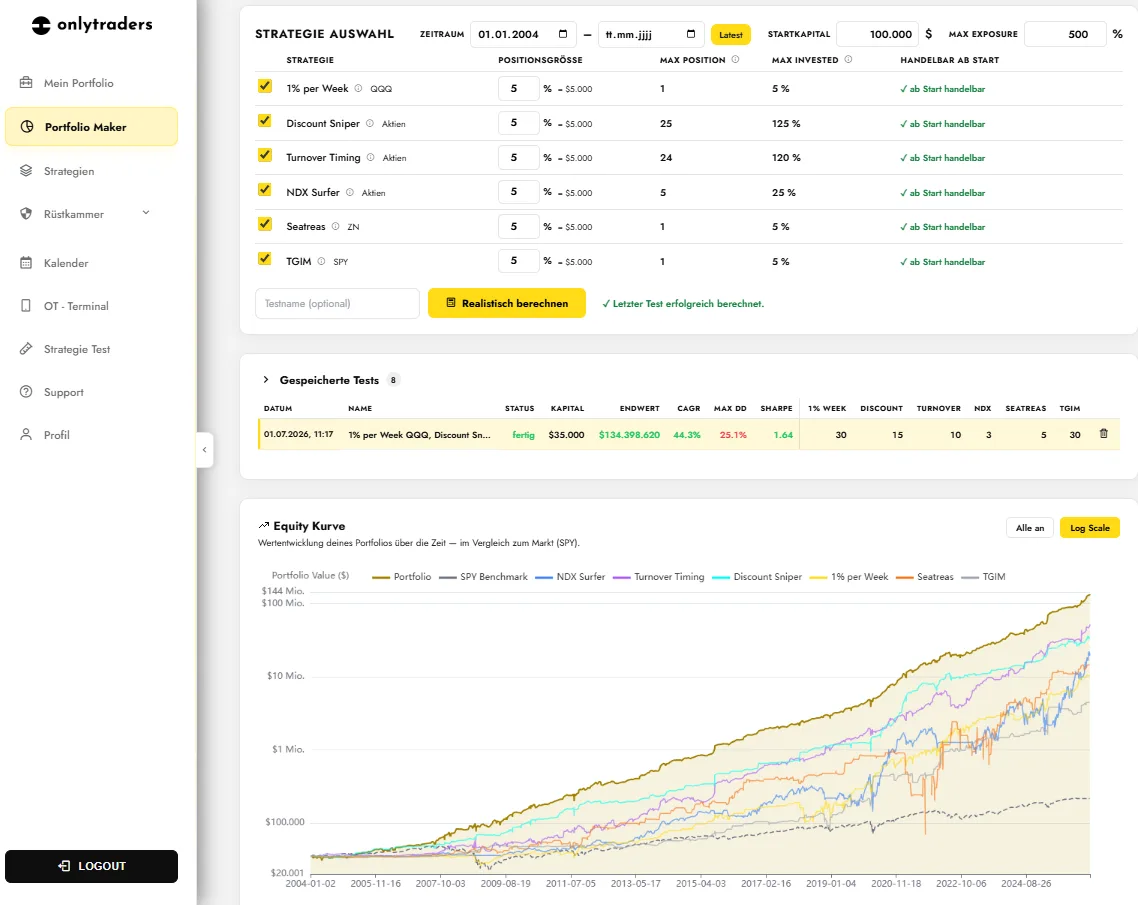

On top of that, after a first preview, the Portfolio Maker will be introduced in more detail. With this powerful tool, every member can see for themselves how the individual strategies in the mix would have behaved with different capital allocations and starting capital.

This portfolio simulation is a milestone. It lets every member assemble their strategy mix to their own needs. One may value capital protection above all else, while another looks for a balanced ratio of return and risk. And of course you can also try “where Lambo,” though I personally wouldn’t recommend it.

Bottom Line

So much for the summer lull: the 100% rule-based strategy mix delivered once again. Real-money performance remains clearly ahead of the key benchmarks while running at a lower drawdown at the same time. The first bigger setback won’t spare us either, but that’s exactly why the mix grows more robust month after month.

If the project interests you, feel free to join our small but fine community. At the very least, sign up for the free Tradingletter to stay in the loop. If you have any questions, reach out at support@onlytraders.com.

Member Wins

As nice as it is that the first seven months are going well for Matthias and me: the most important confirmation of our path with Onlytraders is the success of our members. It proves the reproducibility — and on top of that, one or two people on the team beat our real-money results at times, sometimes by a wide margin.

Who and What Is Onlytraders

For half a year now we’ve been building a community for systematic, emotionless trading strategies with reproducible real-money execution. No hindsight-backtest marketing, but a transparent strategy library that grows month after month. Members get the complete rulebook and the resulting daily buy and sell signals for several stock and index strategies for convenient execution before 15:30 CET, with the OT-Terminal a dedicated order tool for the TWS (Trader Workstation), and access to a community of like-minded people on Discord.

The “we” is so far a 2-man show consisting of Michael Hinterleitner and Matthias Runkel. Both active in the markets for years and convinced that a mix of robust strategies beats any single over-optimized or discretionary strategy.

Our aim: away from gut feeling, toward transparent strategies that anyone can understand, follow and implement with their own risk allocation.

Risk Disclaimer

The performance figures shown in this article refer to a specific historical period and the publicly tracked real-money model account of Onlytraders. Past performance is not a reliable indicator of future results. Trading stocks, futures and other financial instruments involves substantial risk, up to and including the total loss of the capital deployed. Content on onlytraders.com does not constitute investment advice and does not replace an individual consultation with a licensed advisor.